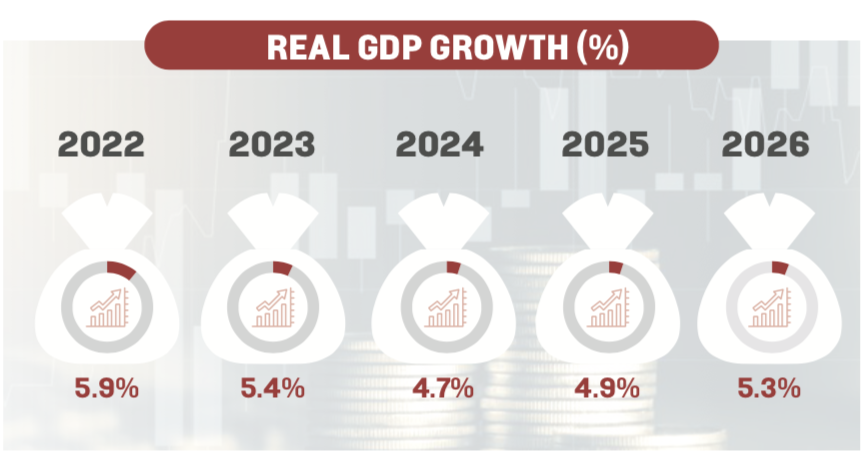

Kenya’s economy grew faster in the first quarter of 2026 than it did a year earlier, with the Kenya National Bureau of Statistics reporting real GDP growth of 5.3 per cent, up from 4.9 per cent in the same period of 2025. Every sector of the economy expanded, though the pace varied widely, and the numbers point to a recovery gathering real momentum rather than a one-off bounce.

The standout performer was accommodation and food services, which grew 14.7 per cent as international arrivals through Jomo Kenyatta and Moi International Airports jumped 13.1 per cent to just over 506,000 visitors. That is a sharp turnaround from the near-flat growth the sector posted a year ago, and it suggests Kenya’s tourism recovery, long promised, is finally translating into consistent numbers rather than seasonal spikes.

Manufacturing also had a strong quarter, growing 4.4 per cent compared with 2.8 per cent last year. The gains were broad-based: sugar output rose 4.4 per cent, soft drink production climbed 7.6 per cent, and vehicle assembly jumped 18.1 per cent. Cement and galvanised sheet production both grew by double digits, a signal that factories tied to construction are running harder to keep up with demand. Banks appear willing to back that expansion too, with credit to manufacturers rising to KSh 588 billion from KSh 566.2 billion a year earlier.

Construction itself grew 6.6 per cent, up from 4.5 per cent, with cement consumption up nearly 18 per cent and credit to the sector rising by close to a third to over KSh 200 billion. Mining and quarrying grew 9.1 per cent, while agriculture, the sector that still employs the largest share of Kenyans, expanded 4.9 per cent, a touch slower than the 5.3 per cent recorded a year ago. Tea, sugarcane and milk deliveries all improved, and cut flower exports grew as well, but coffee and fruit exports fell, pulling down what would otherwise have been a stronger showing from the farm sector.

The financial sector had a good quarter too, expanding 6.3 per cent as borrowing became noticeably cheaper. The Central Bank Rate came down to 8.75 per cent in March, from 10.75 per cent a year earlier, and commercial banks passed some of that relief on: average lending rates fell to 14.70 per cent from 15.77 per cent. Cheaper credit fed through to activity at the Nairobi Securities Exchange, where trading volumes rose by more than a third and the NSE 20 Share Index climbed from 2,227 points to 3,432 points, a strong signal of returning investor confidence.

Not every indicator moved in Kenya’s favour. Inflation ticked up to 4.35 per cent from 3.45 per cent, driven mainly by pricier food and non-alcoholic drinks, and the current account deficit widened sharply, from KSh 70 billion to KSh 120.9 billion, meaning the country is spending more on imports and foreign obligations than it is earning from exports and other inflows. The shilling had a mixed year against major currencies too, holding steady against the US dollar and gaining against the yen, but losing over 11 per cent of its value against the euro and nearly 7 per cent against the pound. It also weakened against the South African rand and regional currencies, including the Ugandan and Tanzanian shillings.

There were softer patches elsewhere in the economy. Mobile money transactions fell by 13.6 per cent even as mobile voice traffic and international bandwidth use both grew, a sign that Kenyans are talking and browsing more but transacting differently, possibly reflecting shifts toward bank-linked digital payments rather than pure mobile money platforms. Electricity generation rose 7.4 per cent, powered largely by a 21 per cent jump in geothermal output, though both wind and solar generation declined during the quarter.

Taken together, the picture is of an economy where the traditionally strong pillars, tourism, manufacturing, construction and finance, are doing the heavy lifting, while agriculture and the currency remain the areas to watch. With interest rates continuing to ease and credit flowing more freely into productive sectors, the coming quarters will show whether this growth can broaden further or whether rising import costs and a wider current account gap start to weigh on the gains.